SENSITIVITY

ANALYSIS

All feasibility studies and valuations using the DCF approach to

measure the rate of return should be subject to a sensitivity analysis.

This will determine the most important variables in the cash flow and

show their comparative rate of change. The normal sensitivity analysis

adjusts the subject variable by +/- 10%. The resulting NPV or IRR using

the equated yield model is recorded in a table or on a graph to show

the sensitivity in terms of absolute amounts or slope of line. All

other variables are held equal. The most commonly analyzed variables

are:

FEASIBILITY STUDIES

Purchase price

or land value

Cost of

construction

Length of

development period

End market

value

EXISTING INVESTMENT

PROPERTIES

Purchase price

End market

value

Rental income

(this can also be use to measure different vacancy rates).

End market

value + rental income.

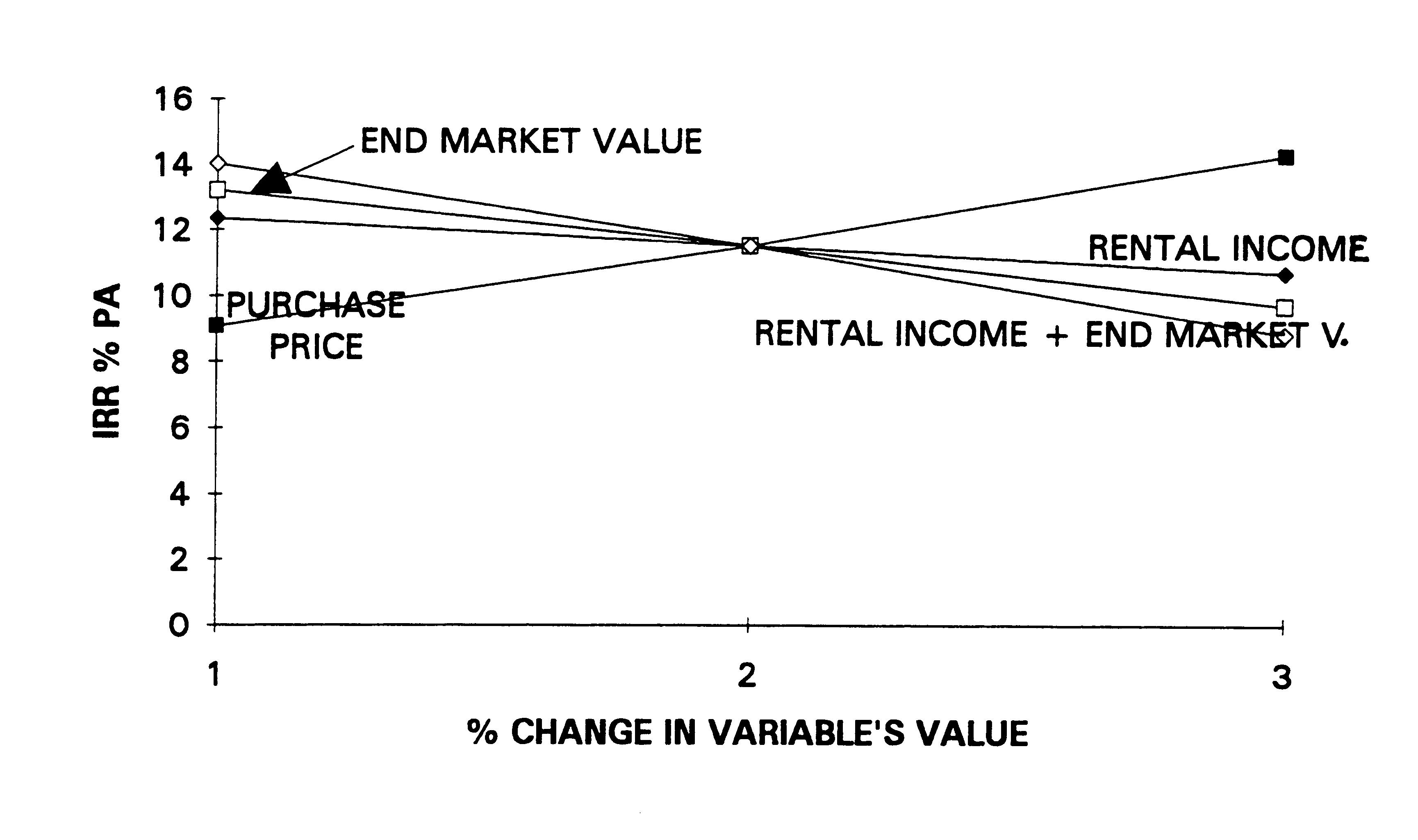

TABLESENSITIVITY ANALYSIS

FOR AN INVESTMENT REPORT OVER SUBJECT PROPERTY The

equated yield rates of return are used to determine the investment's

sensitivity:

VARIABLE VALUE CHANGE

+10%

-10%

PURCHASE PRICE:

9.08%

14.28%

END MARKET VALUE:

13.20%

9.69%

RENTAL INCOME ONLY:

12.34%

10.68%

RENTAL INCOME + END MARKET VALUE:

14.01%

8.83%

The

sensitivity analysis shows that the risk to investment is greatest with

a change in rental income which in turn affects the expected end market

value. The next most important single variable is the purchase price

which is slightly more sensitive than the end market value. Rental

income during the 5 year period is not a very sensitive variable at

all. The above results are better shown on a graph where the

sensitivity of each variable can be observed by it's slope. The steeper

the slope, the more sensitive is the variable - see diagram below:

DIAGRAMSLOPES OF VARIABLES -

SENSITIVITY ANALYSIS

SCENARIOS As

the sensitivity analysis shows, forecasting error can effect both the

feasibility of a project or the value of an existing building.

Therefore, in any situation where the result or value will vary greatly

due to forecasting error it is better for the valuer not to determine a

final answer but instead, provide 3 answers according to the following

scenarios:

Expected (E)

Optimistic (O)

Pessimistic (P)

EXPECTED SCENARIO

The expected scenario is the market's forecast that is, the cash flow

is constructed using data analysed from comparable sales. Where land

values are determined from such a DCF they are market values.

OPTIMISTIC SCENARIO

The optimistic

scenario is that cash flow constructed according to a 10% increase in

rental income and expected end market value. Therefore, the optimistic

scenario in the DCF will determine the highest land value, above market

value.

PESSIMISTIC SCENARIO

The pessimistic scenario is that cash flow which incorporates a 10%

decrease in rental income and expected end market value. Therefore, the

pessimistic scenario will provide the lowest land value, below market

value.Some valuers combine

a number of variable changes in the scenario for example, purchase

price, rental income and end market value. However, this can result in

scenarios which are extremely unlikely and will determine extreme

values.A single statistic

can be calculated for comparison purposes by using the PERT formula: